The Corporate Sustainability Reporting Directive (CSRD), an EU regulatory framework which came into force in January 2023, will replace and enhance the Non-Financial Reporting Directive (NFRD), demanding a broader range of companies to disclose detailed data on environmental, social and governance (ESG) factors, in accordance with the European Sustainability Reporting Standards (“ESRS”). These new rules mark a significant step towards integrating sustainability into corporate strategy, enabling investors, consumers and other stakeholders to make more informed decisions.

Applicability

The CSRD is applicable to large, medium-sized or small companies, including insurance companies, branches of third country undertakings with a net turnover of €40 million, listed companies, qualifying EU subsidiaries of non-EU companies generating over €150 million in the EU market and large companies. The latter, however, must fulfil at least two of the following criteria: having more than 250 employees, having more than €40 million in net turnover and having more than €20 million in total assets.

Although non-listed SMEs and micro-enterprises are excluded from the purview of the CSRD, such companies may still opt to comply with the standards set out in the CSRD on a voluntary basis.

Aim

The primary aim of the CSRD is to ensure that all companies which are subject to the CSRD adopt a harmonised and standardised approach when presenting their reporting under this Directive. In this way, the transparency, quality and content of sustainability information, the company’s flow of money to sustainable activities and ultimately, the company’s trustworthiness in the eyes of the different stakeholders are enhanced.

Reporting

Under the CSRD, reporting is based on the concept of double materiality since companies are not only required to disclose information on how their business activities affect the environment and society in general, but also how their sustainability goals, measures and risks impact the business’ financial health. The CSRD requires that the reported non-financial information must be audited by a third party to ensure its accuracy and reliability. This requirement further enhances the credibility of the reported data.

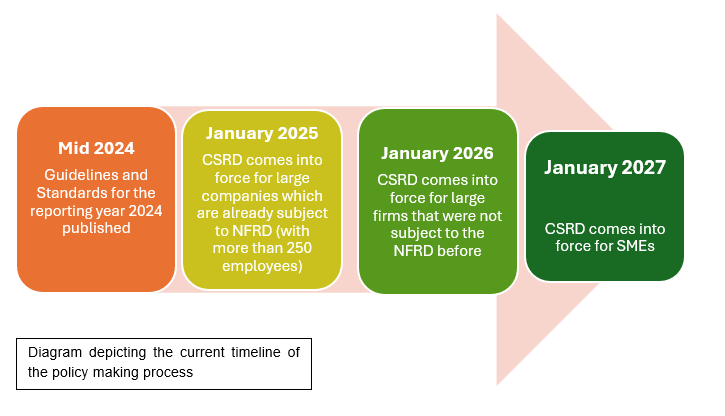

The reporting obligations under this Directive will be rolled out over the coming years, as explained and depicted below:

- Companies that are already subject to the NFRD must produce their first report in 2025. This report should relate to the financial year of 2024.

- Large companies which are not currently subject to the NFRD will have to abide by the CSRD reporting obligations from financial years starting on or after 1st January 2025 and thus must provide their first report in 2026.

- The CSRD will also be applicable to listed SMEs for financial years starting on or after 1st January 2026, although such companies may optout of their CSRD reporting obligations until 2028.

- Standards for SMEs will apply in 2027.

Companies must disclose their ESG data in their Management Reports which are submitted annually. Employees of the company must also be aware of such a report.

The following is a high-level list of the key aspects of non-financial reporting and sustainability matters which companies are expected to include in their Management Report:

a. Environmental Factors

Companies must report on various environmental issues, including:

- Climate Change Mitigation and Adaptation: companies are expected to outline the efforts being made to reduce greenhouse gas emissions as well as the different strategies they have adopted or will adopt in relation to climate change.

- Biodiversity and Ecosystems: companies are required to outline their efforts to protect and restore biodiversity and ecosystems.

- Pollution: companies are required to provide details of the measures which were or will be introduced to reduce pollution.

- Resource Use and Circular Economy: the CSRD requires companies to provide details on their efficient use of resources and the actions that are being taken to implement the circular economy principles.

b. Social Factors

Companies must report on their business model and strategy in relation to social factors as follows:

- Workforce Conditions: companies are expected to provide information on employee well-being, health and safety, working conditions, and their rights.

- Human Rights: companies are required to detail the policies and practices which have been implemented to respect and promote human rights within the company and its supply chain.

- Anti-Corruption and Bribery: companies are required to explain what measures the company has implemented to prevent and address possible corruption and bribery.

- Diversity and Inclusion: companies are required to provide details of the initiatives to promote diversity and inclusion within the workforce, including gender equality.

c. Governance Factors

Companies must report on governance-related disclosures including:

- Board Diversity: companies are required to provide details of the board composition and the diversity of the board of directors.

- Executive Pay: companies are expected to provide details of the remuneration policies for their executives and how they align with sustainability goals.

- Sustainability Risk Management: companies are to provide details on how the company ensures that the board of directors is overseeing sustainability risks as well as opportunities must also be provided.

- Ethical Business Practices: CSRD requires companies to provide details on the internal policies and practices in place that promote ethical behaviour and integrity.

Compliance with the CSRD

Non-compliance by companies can result in the payment of penalties. There are three possible penalties, including a public statement about the breach, an order on the name of the entity demanding a change in conduct and lastly, financial sanctions.

Member States enjoy the discretion to determine the type of penalty to be imposed on the company which failed to comply with the requirements under the CSRD. However, administrative and pecuniary sanctions should be “effective, proportionate and dissuasive.” Such sanctions should also consider the seriousness and duration of the breach, the importance of profits gained, or losses avoided through the breach, the degree of responsibility, the financial strength of the company, any losses which were sustained by third parties, the level of cooperation by the company, and any previous similar infringements.

Another consequence of insufficient reporting is the possible loss of investments. Sustainability-related issues can affect the company’s performance which may ultimately push away potential investors. In addition, compliance with the CSRD can bring more clarity to the reporting process which can ultimately attract green investments.

There is no doubt that the CSRD is playing a crucial role in promoting sustainable business practices across Europe. This framework is an important step in ultimately achieving the objectives of the European Green Deal, the EU’s ambitious strategy for reaching climate neutrality by 2050.

This document does not purport to give legal, financial or tax advice. Should you require further information or legal assistance, please do not hesitate to contact Mr Claudio Xerri